As additional inventory is purchased during the period, the cost of those goods is added to the merchandise inventory account. Normally, no significant adjustments are needed at the end of the period (before financial statements are prepared) since the inventory balance is maintained to continually parallel actual counts. The inventory at period end should be $7,872, requiring an entry to increase merchandise inventory by $4,722. Journal entries are not shown, but the following calculations provide the information that would be used in recording the necessary journal entries. Cost of goods sold was calculated to be $8,283, which should be recorded as an expense.

Specific Identification

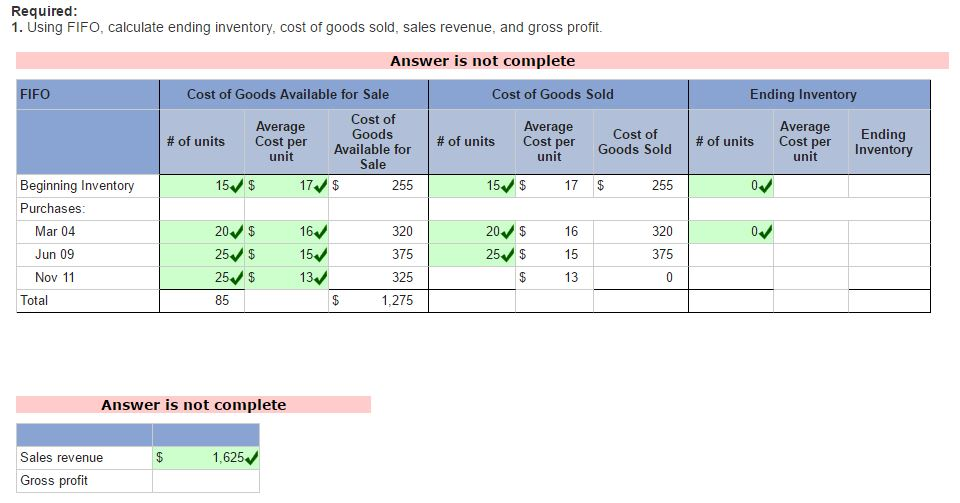

Therefore, the method chosen to value inventory and COGS will directly impact profit on the income statement as well as common financial ratios derived from the balance sheet. First in, first out (FIFO) assumes that the oldest items purchased by the company were used in the production of the goods that were sold earliest. Under FIFO, the cost of the oldest items purchased are allocated first to COGS, while the cost of more recent purchases are allocated to ending inventory—which is still on hand at the end of the period. At its most basic level, ending inventory can be calculated by adding new purchases to beginning inventory, then subtracting the cost of goods sold (COGS).

Calculations for Inventory Adjustment, Periodic/First-in, First-out (FIFO)

The inventory valuation method chosen by management impacts many popular financial statement metrics. Inventory-related income statement items include the cost of goods sold, gross profit, and net income. Current assets, working capital, total assets, and equity come from the balance sheet. All of these items are important components of financial ratios used to assess the financial health and performance of a business. One method for calculating ending inventory is by conducting a physical count of the quantity of each item in inventory. This involves physically counting the items and then multiplying the quantities by their respective unit costs.

Would you prefer to work with a financial professional remotely or in-person?

- Auditors may require that companies verify the actual amount of inventory they have in stock.

- Once those units were sold, there remained30 more units of the beginning inventory.

- Doing a count of physical inventory at the end of an accounting period is also an advantage, as it helps companies determine what is actually on hand compared to what’s recorded by their computer systems.

- Whenapplying perpetual inventory updating, a second entry made at thesame time would record the cost of the item based on FIFO, whichwould be shifted from merchandise inventory (an asset) to cost ofgoods sold (an expense).

It involves calculating the gross profit ratio by dividing the gross profit by net sales. This ratio is then applied to the net sales during the accounting period to estimate the cost of goods sold. Subtracting the estimated cost of goods sold from the cost of goods available for sale gives the estimated ending inventory.

What is the approximate value of your cash savings and other investments?

Figure 10.18 shows the gross margin resulting from the LIFOperpetual cost allocations of $7,380. Figure 10.16 shows the gross margin, resulting from the FIFOperpetual cost allocations of $7,200. The gross margin, resulting from the LIFO periodic cost allocations of $9,360, is shown in Figure 10.10. The gross margin, resulting from the FIFO periodic cost allocations of $7,200, is shown in Figure 10.8.

Definition of Specific Identification

Figure 10.18 shows the gross margin resulting from the LIFO perpetual cost allocations of $7,380. Figure 10.16 shows the gross margin, resulting from the FIFO perpetual cost allocations of $7,200. The next step is to assign one of the three valuation methods to the items in COGS and ending inventory. Let’s assume the 200 items in beginning calculating the issue price of a bond using the npv function in excel extra credit inventory, as of 7/31, were all purchased previously for $20. Compute gross profit earned by the company for each of the four costing methods in part 3. Let’s return to The Spy Who Loves You Corporation data todemonstrate the four cost allocation methods, assuming inventory isupdated on an ongoing basis in a perpetual system.

Another approach is to use the quantities recorded in the company’s inventory system to calculate ending inventory. These quantities are multiplied by the actual unit costs based on the company’s chosen cost flow assumption, such as FIFO or weighted-average. The purchases costs, which include the purchase price less any sales discounts, insurance in transit, freight charges, and taxes are included in the ending inventory along with other related direct costs. These costs are added to the total cost of the goods available for sale (the beginning inventory). However, prices do not remain stable, and so accountants have developed alternative methods to attach costs to inventory items.

Multiply the quantities of each item in inventory by their respective unit costs. It is important to determine ending inventory as it converts book value to a tangible number. It also determines whether total revenue is higher or lower than the cost of goods sold, which in turn affects net income. This is usually done by taking a physical inventory at least once a year, usually at year-end.

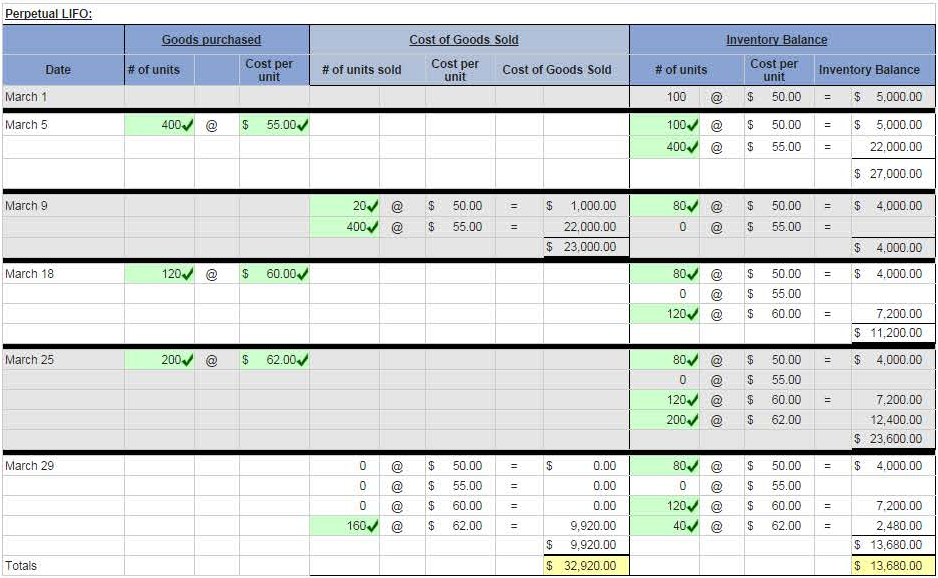

Whenapplying perpetual inventory updating, a second entry would be madeat the same time to record the cost of the item based on the AVGcosting assumptions, which would be shifted from merchandiseinventory (an asset) to cost of goods sold (an expense). The LIFO costing assumption tracks inventory items based on lots of goods that are tracked, in the order that they were acquired, so that when they are sold, the latest acquired items are used to offset the revenue from the sale. The following cost of goods sold, inventory, and gross margin were determined from the previously-stated data, particular to LIFO costing. The FIFO costing assumption tracks inventory items based on segments or lots of goods that are tracked, in the order that they were acquired, so that when they are sold, the earliest acquired items are used to offset the revenue from the sale.

Leave a Reply